Most people think of Type 2 diabetes, hypertension, and heart disease as health problems. They’re not wrong — but they’re only seeing half the picture. These conditions are also financial emergencies hiding in plain sight, quietly eating away at savings, earning potential, and retirement plans for 20, 30, even 40 years. And unlike a sudden job loss or a stock market crash, the financial damage builds so slowly that most people never see it coming until it’s too late.

Key Takeaways

- A person diagnosed with Type 2 diabetes in their 40s faces decades of compounding medical costs — regardless of where they live or what healthcare system covers them.

- Up to half of those costs come from managing complications, not the disease itself.

- People with diabetes in the United States spend roughly 2.6 times more on healthcare than people without diabetes.

- Three lifestyle changes — weight, movement, and sleep — have the strongest evidence for preventing the condition.

- Prevention programmes have been shown to cut diabetes risk by more than 50% in high-risk individuals.

Why This Is a Financial Problem, Not Just a Health Problem

Here’s a framing you almost never see in personal finance coverage: chronic lifestyle diseases don’t just change how you live. They rewrite your financial plan.

Think about how a standard financial plan works. You earn a salary, you save a portion, you invest, and eventually you retire comfortably. That plan assumes a few things: that your income stays reasonably stable, that your expenses stay predictable, and that your working years aren’t cut dramatically short.

A chronic condition quietly dismantles all three of those assumptions — through costs that arrive slowly, in layers, and often feel manageable in isolation.

The Costs Nobody Adds Up

When people think of the cost of diabetes, they might think of a monthly prescription. That’s one layer. But here’s what actually accumulates over time:

- Daily medications — often for life, and increasing in complexity as the disease progresses

- Regular blood tests and doctor visits — typically multiple times per year

- Specialist appointments — endocrinologists, cardiologists, ophthalmologists, kidney specialists

- Diabetes supplies — monitoring devices, testing strips, insulin delivery equipment

- Treating complications — which is where the real costs explode

The complication costs are the financial trap most people miss entirely. Around 48 to 64 percent of lifetime medical costs for someone with diabetes come not from managing blood sugar, but from treating the things diabetes causes: heart disease, kidney damage, nerve damage, and vision problems. Each of those complications comes with its own treatment costs, its own specialist visits, and in serious cases, its own hospitalisation bills.

Related: The Evolution of Money: From Clay Tablets to Digital Currency

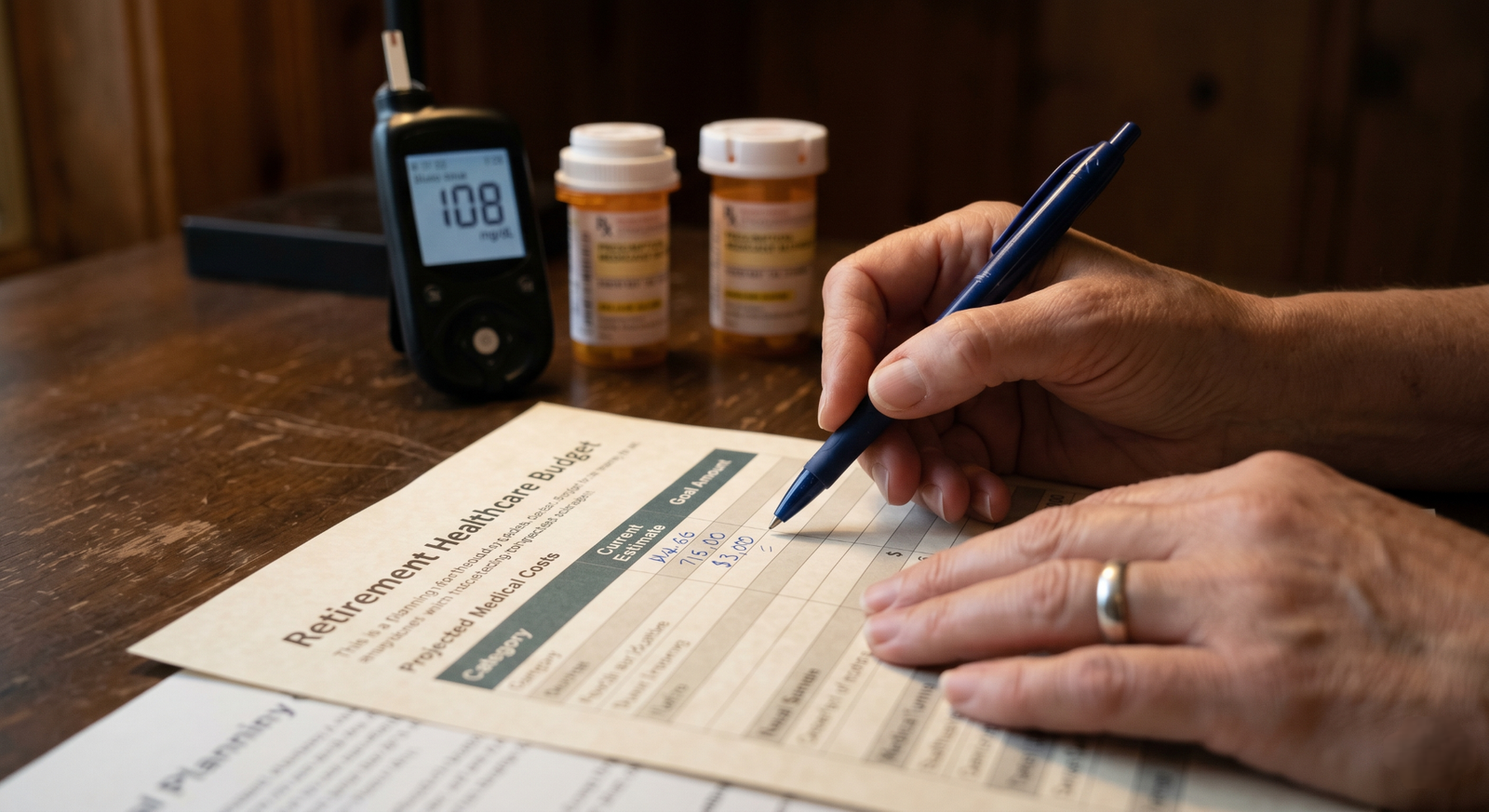

What the Lifetime Numbers Actually Look Like

Research tracking the true lifetime medical costs of treating Type 2 diabetes and its complications has found consistent patterns across high-income countries. People diagnosed in their 20s, 30s, and 40s face the heaviest financial burden — simply because they live with the condition for longer.

In countries where patients pay directly for healthcare, lifetime medical costs for someone diagnosed in middle age can run well into six figures. In countries with universal or state-funded healthcare, those costs shift rather than disappear: they fall on the state, on employers, and on individuals through reduced income, lost working hours, and out-of-pocket spending on things that coverage doesn’t include — specialist visits, devices, and the many small costs that add up month after month.

Wherever you live, the core dynamic is the same. These figures cover only direct medical expenses. They exclude lost income, reduced working hours, and the cost of care when the condition becomes severe.

To put it simply: getting diagnosed with Type 2 diabetes in your 40s typically means taking on the equivalent of a small mortgage in future costs — one that accumulates silently over decades.

The Indirect Costs Are Just as Serious

The major contributors to indirect costs include reduced employment due to disability, presenteeism — which means showing up to work but being too unwell to perform fully — and lost productivity from premature deaths.

In everyday language: chronic illness doesn’t just cost you money in medical bills. It costs you money in promotions you don’t get, projects you can’t take on, hours you can’t work, and — in serious cases — years of earning you lose entirely. For anyone who is self-employed or in a job without strong disability protection, these indirect costs can be far more devastating than the medical bills themselves.

Annual medical spending for people with diabetes is more than twice that of people without the condition. Over 30 or 40 years, that gap compounds into a financial chasm.

How Prevention Changes the Numbers

Here is where the story shifts — because lifestyle diseases are not inevitable, and the financial return on prevention is measurable and significant.

Multiple large studies show that a structured lifestyle change programme focused on healthy eating and physical activity can reduce the risk of Type 2 diabetes by more than 50% for people at high risk.

The three lifestyle changes with the strongest evidence for both health outcomes and long-term cost avoidance are:

1. Weight Management

Losing around 7% of body weight through changes in physical activity and diet lowered the risk of developing Type 2 diabetes by almost 60% over three years in one large study. For a person weighing 90kg, that’s roughly 6kg — a modest, achievable target, not a dramatic transformation.

The financial logic is straightforward: every year you delay or avoid a diabetes diagnosis is a year without the compounding costs that diagnosis brings.

2. Regular Physical Activity

Research tracking older adults over nearly seven years found that every 2,000 additional daily steps was associated with a 12% reduction in Type 2 diabetes risk. You don’t need a gym membership or a complex exercise programme. Walking — consistently, daily — has measurable, evidence-backed impact on your risk profile and, by extension, your lifetime financial exposure.

Physical inactivity is consistently linked to a significantly higher risk of Type 2 diabetes, with studies showing increased risk ranging from 20% to over 50% depending on how inactive a person is. These aren’t dramatic thresholds. They’re the kind of gradual drift that happens to people who stay mostly sedentary through their 30s and 40s.

Related: Don’t Let Scammers Steal Your Money

3. Sleep Consistency

This is the lifestyle factor that almost no financial health content ever mentions — but the evidence is hard to ignore.

A large 2024 study found that people whose nightly sleep varied by more than an hour had a 34% higher risk of developing Type 2 diabetes. Separately, research has shown that consistently sleeping under 5 hours can raise risk by up to 41–45% compared to those getting 7–8 hours.

There is now established evidence for a connection between sleep duration and Type 2 diabetes risk, with both short sleep (under 6 hours) and long sleep (over 9 hours) each associated with up to a 50% increase in risk. International diabetes care guidelines published in 2025 now place sleep on the same level as diet and exercise as a prevention tool — a significant shift from previous guidance.

The optimal appears to be around 7 hours per night — consistently, at regular times. This isn’t a wellness tip. For someone in their 30s or 40s, it’s a financial planning decision.

What Investing in Prevention Actually Costs

Research consistently shows that the financial return from diabetes prevention becomes measurable within a few years — not decades. In other words, the relatively small upfront effort of structured prevention — a better diet, regular movement, and consistent sleep — pays for itself in avoided medical costs well within a normal financial planning horizon.

To put that in perspective: the cost of eating more whole foods and walking 30 minutes a day is effectively zero compared to the cost of managing diabetes and its complications for 20 or 30 years.

Between 48% and 64% of lifetime medical costs for a person with diabetes relate to complications such as heart disease and stroke — not the disease management itself. Every year of prevention is a year of compounding those costs avoided.

The Window That Closes

The most uncomfortable truth in all of this is timing. The lifestyle changes that carry the strongest return — weight management, movement, sleep — are most effective in your 30s and 40s, before a diagnosis is made and before complications begin to accumulate.

Research also shows that healthcare costs for people who eventually develop diabetes start rising years before the formal diagnosis is made. The window for high-impact prevention is not after a diagnosis — it’s the decade before one.

Most personal finance advice tells you to save more, invest wisely, and plan carefully for retirement. All of that matters. But the single highest-return financial decision many people in their 30s and 40s can make is protecting the earning capacity and health that makes every other financial decision possible.

Your body is your most valuable long-term asset. Treating it like one is not a lifestyle choice. It’s a financial strategy.